econometrics_application.ipynb

Optimal Transport in linear ICA applied to Econometrics

In this application we test our methodology to find ICs in a simulated price discovery case between distinct markets

import numpy as np

import torch

import scipy.stats

import matplotlib.pyplot as plt

from scipy.optimize import linear_sum_assignment

from wasserstein_ica import WassersteinICA

import matplotlib.pyplot as plt

import matplotlib as mpl

# Define a consistent Thesis Theme

def set_thesis_theme():

# Academic, colorblind-friendly palette

# Blue, Orange, Green, Red, Purple, Brown

thesis_colors = ['#0173B2', '#DE8F05', '#029E73', '#D55E00', '#CC78BC', '#CA9161']

mpl.rcParams.update({

# Figure and Layout

'figure.figsize': (8, 5),

'figure.dpi': 300, # High resolution for print

'axes.prop_cycle': mpl.cycler(color=thesis_colors),

# Grid lines (light and unobtrusive)

'axes.grid': True,

'grid.alpha': 0.3,

'grid.linestyle': '--',

'axes.axisbelow': True, # Grid goes behind data

# Spines (remove top and right borders for a cleaner look)

'axes.spines.top': False,

'axes.spines.right': False,

# Fonts and Text

'font.size': 11,

'axes.titlesize': 13,

'axes.labelsize': 12,

'xtick.labelsize': 10,

'ytick.labelsize': 10,

# Legends

'legend.frameon': False, # No box around the legend

'legend.fontsize': 10,

# Lines

'lines.linewidth': 2.0

})

# Run this before plotting

set_thesis_theme()

def apply_economic_constraints(W_est, W_white):

"""

Post-process the statistical ICA output to enforce economic meaning.

Addresses the critique that standard ICA results are permutation/sign indefinite.

We apply:

1. Dominant Diagonal: The shock impacting Market i the most is labeled Shock i.

2. Positive Spillover: Structural shocks are normalized to have positive effects.

Args:

W_est (Torch Tensor): Unmixing matrix from ICA (Whitened space).

W_white (Torch Tensor): Whitening matrix used.

Returns:

B_identified (Numpy Array): The economically identified Mixing Matrix.

"""

# 1. Recover the Raw Mixing Matrix (B_raw)

# The total estimated unmixing is W_tot = W_est @ W_white

# The mixing matrix B is the inverse: X = B * S

W_total = torch.matmul(W_est, W_white)

B_raw = torch.linalg.inv(W_total).cpu().numpy()

# 2. Permutation Constraint (Dominant Diagonal)

# We use the Hungarian Algorithm (linear_sum_assignment) to match

# Shocks (columns) to Markets (rows) such that the diagonal magnitude is maximized.

# We pass negative absolute values because the algorithm minimizes cost.

row_ind, col_ind = linear_sum_assignment(-np.abs(B_raw))

# Reorder the columns (shocks) of B

B_permuted = B_raw[:, col_ind]

# 3. Sign Constraint (Positive Impact)

# Ensure the diagonal elements are positive (B_ii > 0).

# If B_ii is negative, we assume we found the "negative" shock and flip the column.

diagonals = np.diag(B_permuted)

sign_corrections = np.sign(diagonals)

# Broadcast multiplication to flip columns where sign is negative

B_identified = B_permuted * sign_corrections[np.newaxis, :]

return B_identified

# ==============================================================================

# EXPERIMENT SETUP (Replicating Zema & Cordoni DGP)

# ==============================================================================

# Simulation Settings

N_SIMULATIONS = 500 # Number of Monte Carlo runs

T_SAMPLES = 5000 # Observations per run (Daily returns)

N_MARKETS = 3

DEVICE = torch.device("cuda" if torch.cuda.is_available() else "cpu")

# Define the "True" Structure

# We target Information Shares: [0.12, 0.24, 0.64]

# Assuming a standard VECM where the orthogonal complement to beta is [1, 1, 1],

# The IS is proportional to the squared column sums of B.

target_is = np.array([0.12, 0.24, 0.64])

psi = np.array([1.0, 1.0, 1.0]) # Long-run impact vector

# Construct a True Mixing Matrix B that yields these shares.

# For simplicity, we use a diagonal B scaled by sqrt(target).

# (Note: Even with a diagonal B_true, the ICA has to work because we whiten the data,

# effectively destroying the structure, and ICA must rotate it back).

B_true = np.diag(np.sqrt(target_is))

print(f"Running Experiment on {DEVICE}...")

print(f"Target True IS: {target_is}")

print(f"Constraint Mode: Dominant Diagonal & Positive Signs")

results_is = []

Running Experiment on cuda...

Target True IS: [0.12 0.24 0.64]

Constraint Mode: Dominant Diagonal & Positive Signs

for sim in range(N_SIMULATIONS):

# --- A. Data Generation (Student-t Innovations) ---

# Independent shocks with degrees of freedom 5, 6, 7 (Heavy tails)

s1 = np.random.standard_t(df=5, size=T_SAMPLES)

s2 = np.random.standard_t(df=6, size=T_SAMPLES)

s3 = np.random.standard_t(df=7, size=T_SAMPLES)

# Stack and Normalize to unit variance (Standard ICA assumption)

S = np.vstack([s1, s2, s3])

S = S / S.std(axis=1, keepdims=True)

# Mix the signals

X_np = B_true @ S

X_torch = torch.tensor(X_np, dtype=torch.float32, device=DEVICE)

# --- B. Wasserstein ICA ---

model = WassersteinICA(X_torch)

model.whiten()

dim = X_torch.shape[0]

num_restarts = min(dim * 4, 150)

#

# OPTIMIZATION PHASE 1: Deflationary SGD

# Sequentially extract components to form a robust initialization matrix

W_init_list = []

prev_components = torch.empty((0, dim), device=DEVICE)

for k in range(dim):

w_k, _ = model.optimize_wasserstein2(

prev_components=prev_components,

continuous=True,

max_iter=200,

lr=0.1,

n_restarts=num_restarts

)

W_init_list.append(w_k)

prev_components = torch.cat([prev_components, w_k.unsqueeze(0)], dim=0)

W_init = torch.stack(W_init_list)

# OPTIMIZATION PHASE 2: Symmetric Stiefel Optimization

# Refine the initial matrix simultaneously on the Stiefel manifold

W_opt = model.optimize_symmetric(

n_components=dim,

optimizer='stiefel',

init_w=W_init,

use_sinkhorn=False,

max_iter=300,

lr=1.0

)

# --- C. Economic Identification ---

B_final = apply_economic_constraints(W_opt, model.W_white)

# --- D. Calculate Information Share ---

# Calculate the long-run impact of each shock: Psi * B_column

# Since Psi=[1,1,1], this is just the column sum.

impacts = psi @ B_final

# Variance contribution = impact^2

variances = impacts ** 2

# Information Share = Variance / Total Variance

estimated_is = variances / np.sum(variances)

results_is.append(estimated_is)

if (sim + 1) % 10 == 0:

print(f"Simulation {sim+1}/{N_SIMULATIONS} completed.")

Simulation 10/500 completed.

Simulation 20/500 completed.

Simulation 30/500 completed.

Simulation 40/500 completed.

Simulation 50/500 completed.

Simulation 60/500 completed.

Simulation 70/500 completed.

Simulation 80/500 completed.

Simulation 90/500 completed.

Simulation 100/500 completed.

Simulation 110/500 completed.

Simulation 120/500 completed.

Simulation 130/500 completed.

Simulation 140/500 completed.

Simulation 150/500 completed.

Simulation 160/500 completed.

Simulation 170/500 completed.

Simulation 180/500 completed.

Simulation 190/500 completed.

Simulation 200/500 completed.

Simulation 210/500 completed.

Simulation 220/500 completed.

Simulation 230/500 completed.

Simulation 240/500 completed.

Simulation 250/500 completed.

Simulation 260/500 completed.

Simulation 270/500 completed.

Simulation 280/500 completed.

Simulation 290/500 completed.

Simulation 300/500 completed.

Simulation 310/500 completed.

Simulation 320/500 completed.

Simulation 330/500 completed.

Simulation 340/500 completed.

Simulation 350/500 completed.

Simulation 360/500 completed.

Simulation 370/500 completed.

Simulation 380/500 completed.

Simulation 390/500 completed.

Simulation 400/500 completed.

Simulation 410/500 completed.

Simulation 420/500 completed.

Simulation 430/500 completed.

Simulation 440/500 completed.

Simulation 450/500 completed.

Simulation 460/500 completed.

Simulation 470/500 completed.

Simulation 480/500 completed.

Simulation 490/500 completed.

Simulation 500/500 completed.

#==============================================================================

# RESULTS TABLE

# ==============================================================================

results_is = np.array(results_is)

mean_is = np.mean(results_is, axis=0)

std_is = np.std(results_is, axis=0)

print("\n" + "="*60)

print(f"{'Market / Source':<15} | {'True IS':<10} | {'Est. IS (Mean)':<15} | {'Std Dev':<10}")

print("-" * 60)

for i in range(N_MARKETS):

print(f"Market {i+1:<14} | {target_is[i]:<10.4f} | {mean_is[i]:<15.4f} | {std_is[i]:<10.4f}")

print("="*60)

============================================================

Market / Source | True IS | Est. IS (Mean) | Std Dev

------------------------------------------------------------

Market 1 | 0.1200 | 0.1212 | 0.0170

Market 2 | 0.2400 | 0.2386 | 0.0249

Market 3 | 0.6400 | 0.6402 | 0.0273

============================================================

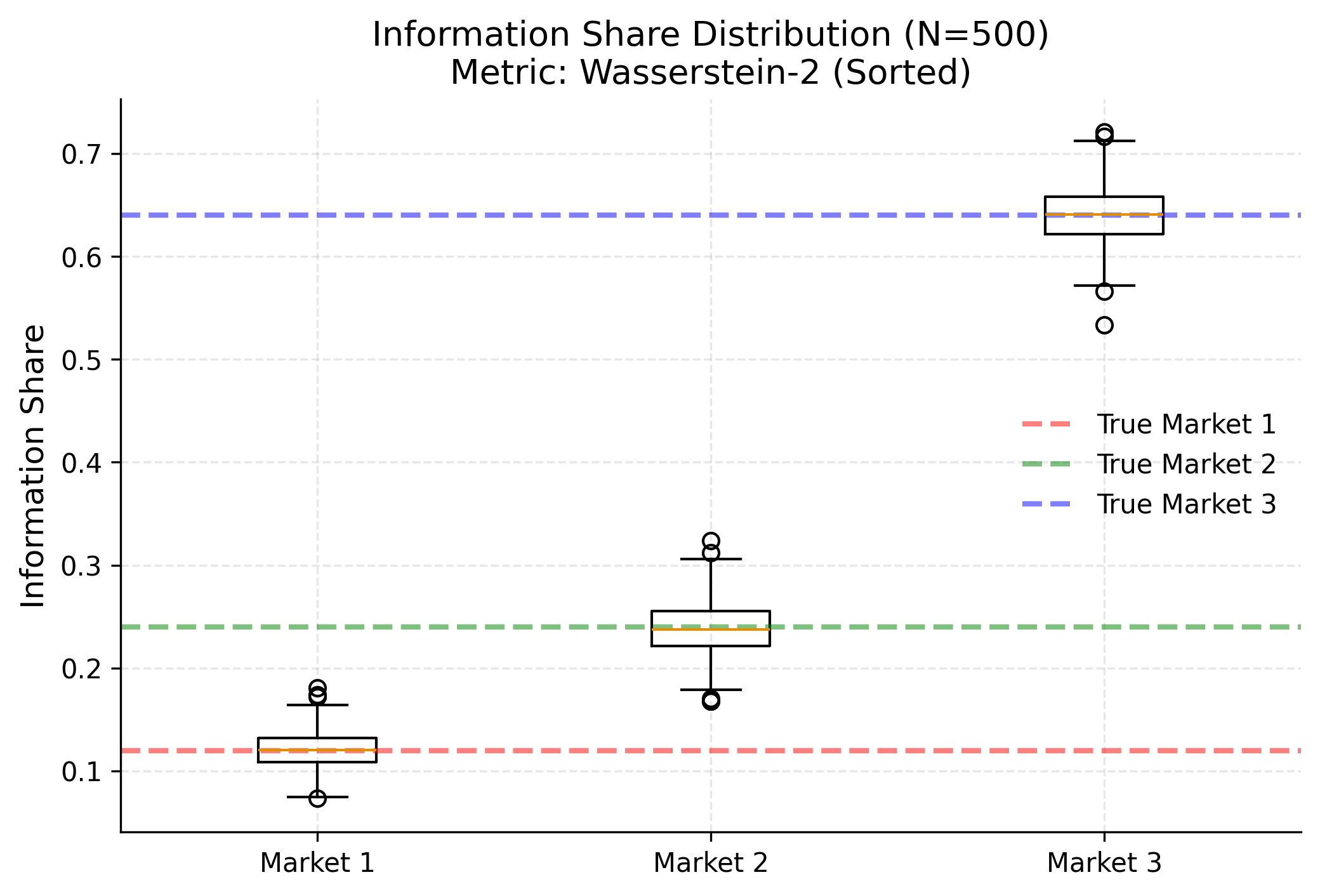

plt.figure(figsize=(8, 5))

plt.boxplot(results_is, tick_labels=['Market 1', 'Market 2', 'Market 3'])

plt.title(f"Information Share Distribution (N={N_SIMULATIONS})\nMetric: Wasserstein-2 (Sorted)")

plt.ylabel("Information Share")

# Draw True IS lines

colors = ['red', 'green', 'blue']

for i in range(3):

plt.axhline(target_is[i], color=colors[i], linestyle='--', alpha=0.5, label=f'True Market {i+1}')

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

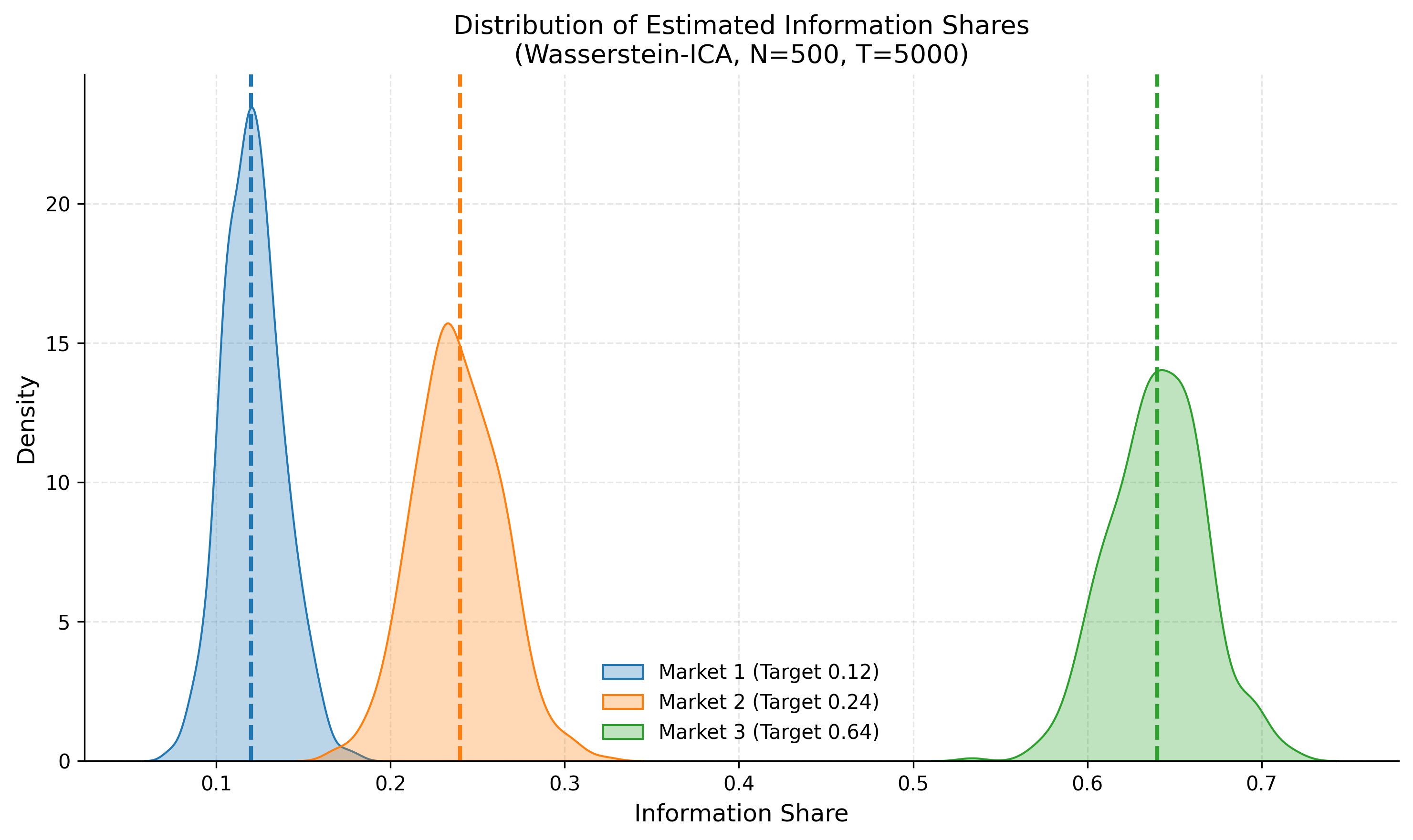

import matplotlib.pyplot as plt

import seaborn as sns # Optional, for nicer plots

# Plotting the distributions of Estimated Information Shares

plt.figure(figsize=(10, 6))

colors = ['#1f77b4', '#ff7f0e', '#2ca02c'] # Blue, Orange, Green

labels = ['Market 1 (Target 0.12)', 'Market 2 (Target 0.24)', 'Market 3 (Target 0.64)']

targets = [0.12, 0.24, 0.64]

for i in range(3):

# Extract the column for Market i across all 500 simulations

data = results_is[:, i]

# Plot Histogram/KDE

sns.kdeplot(data, color=colors[i], fill=True, alpha=0.3, label=labels[i])

plt.axvline(targets[i], color=colors[i], linestyle='--', linewidth=2)

plt.title(f'Distribution of Estimated Information Shares\n(Wasserstein-ICA, N={N_SIMULATIONS}, T={T_SAMPLES})')

plt.xlabel('Information Share')

plt.ylabel('Density')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

Economic Identification Strategy

Unlike the statistical output of raw ICA, which is permutation and sign indeterminate, we impose two strict economic constraints to recover the structural parameters:

- Dominant Diagonal (Permutation): We strictly enforce that the structural shock assigned to Market $i$ must be the one that contributes the maximum variance to that specific market. This is implemented via the Hungarian Algorithm to solve the assignment problem.

- Positive Impact (Sign): We assume positive spillovers, meaning a structural innovation (good news) must have a positive initial impact on its own price. Negative coefficients are sign-flipped.