Interbank Decisions and Margins of Stability: an Agent-Based Stock-Flow Consistent Approach

This repository contains the files to replicate the simulations of the paper "Interbank Decisions and Margins of Stability: an Agent-Based Stock-Flow Consistent Approach" published in the Journal of Economic Dynamics and Control.

To contact me: Jessica Reale

Please cite this article as: Reale J. (2024), Interbank Decisions and Margins of Stability: an Agent-Based Stock-Flow Consistent Approach, Journal of Economic Dynamics and Control, 160, 104822.

What you can find in this repository

The src folder contains the following elements:

-

the main module of this project

IMS.jlwhich includes:- what happens at each simulation step (model_step! function);

- several model-based functions that update credit and interbank market matching and interbank interest rates.

-

the scripts to run the model:

- the script to execute the model without data saving nor parallel replications

run.jl; - the script to execute the model with parallelised replications and data saving

run_complex.jl.

- the script to execute the model without data saving nor parallel replications

-

the model characteristics within the

modelfolder that includes:- the model initialisation file

init.jl; - the set of exogenous parameters and corresponding value

params.jl; - the mutable structs of each agent type that defines properties and variables

structs.jl; - some functions of general utility in

utils.jlwhich also includes the Stock-Flow consistency checks performed at each simulation step; - a folder

SFCwhere all behavioural rules are defined for each class of agents/sectors:

- the model initialisation file

-

the scripts to load the data collected and generate plots

plots; -

the scripts to run sensitivity analysis on parameter values and plot the results

sensitivity-analysis.

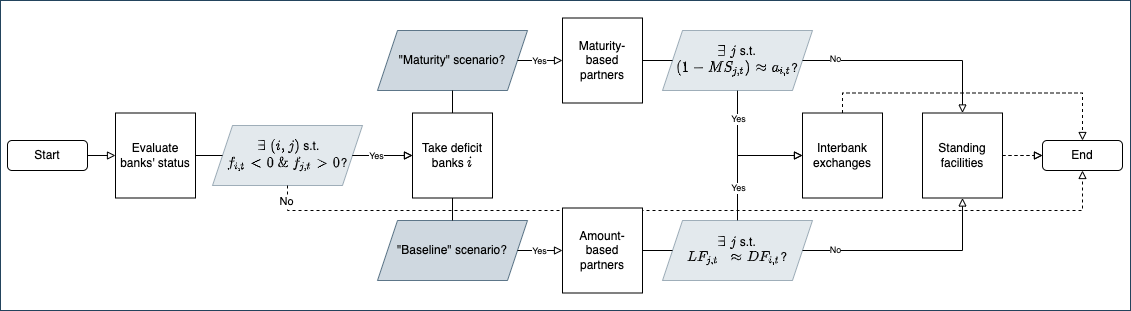

Interbank matching mechanisms

Simulations

We run the simulations over two scenarios (scenario) diversified by the interbank matching protocol. Each scenario is shocked with three experiments. The table below summarises the shocks we implement.

Shocks shock |

Variables | Step shock_incr |

|---|---|---|

| Missing-shock | – | – |

| Corridor-shock | icbl, icbd, icbt += 0.005 |

every 300 steps |

| Width-shock | icbl, icbt += 0.005 |

every 300 steps |

| Uncertainty-shock | PDU += 0.2 |

every 300 steps |

Sensitivity analysis

We perform sensitivity tests on ten parameters:

| Parameter | Range | Description |

|---|---|---|

model.r |

{0.9, 1.1, 1.3} | government debt-to-GDP ratio |

model.δ |

{0.05, 0.5, 1.0} | capital depreciation |

model.l |

{0.03, 0.5, 1.0} | share of non-performing loans |

model.γ |

{0.1, 0.5, 1.0} | households’ leverage |

model.gd |

{0.1, 0.5, 1.0} | proportion of wages deposited |

model.m1 |

[0.0:0.1:1.0] | RSF risk factor on short-term loans |

model.m2 |

[0.0:0.1:1.0] | RSF risk factor on medium-term loans |

model.m3 |

[0.0:0.1:1.0] | RSF risk factor on long-term government bonds |

model.m4 |

[0.0:0.1:1.0] | ASF risk factor on deposits |

model.m5 |

[0.0:0.1:1.0] | ASF risk factor on term interbank loans |